Options traders distinguish between actual volatility, recorded and measured from data, and implied volatility. The latter term comes from solving the options models using price and the various known inputs. Typically volatility is the only input term that must be estimated. High implied volatility means that traders of options are incorporating uncertainty in their estimates. With this in mind…

Get ready for maximum potential volatility in a single trading hour!

It starts Thursday afternoon, when we will get the results on participation in the Greek debt swap only an hour before the market close. Before the opening on Friday, we will get the most important economic news of the month, the employment situation report.

The Data

We all want to know whether the economy is improving and, if so, by how much. Employment is the key metric since it is fundamental for consumption, corporate profits, tax revenues, deficit reduction, and financial markets.

We would like to know the net addition of jobs in the month of February.

To provide an estimate of monthly job changes the BLS has a complex methodology that includes the following steps:

- An initial report of a survey of establishments. Even if the survey sample was perfect (and we all know that it is not) and the response rate was 100% (which it is not) the sampling error alone for a 90% confidence interval is +/- 100K jobs.

- The report is revised to reflect additional responses over the next two months.

- There is an adjustment to account for job creation — much maligned and misunderstood by nearly everyone.

- The final data are benchmarked against the state employment data every year. This usually shows that the overall process was very good, but it led to major downward adjustments at the time of the recession. More recently, the BLS estimates have been too low. (See my preview from last month for a more detailed account of this, along with supporting data).

I think the BLS is honest and does a good job, which seems to put me in a small minority of observers. Despite this support, I question the general concept. The BLS tries to estimate total employment in one month, total employment in another, and subtract the two to determine the difference. When you are talking total payroll employment of over 130 million jobs, even small errors are in the range of 100K jobs or more. Meanwhile, smaller discrepancies from expectations are unwisely viewed as significant.

Competing Estimates

The BLS report is really an initial estimate, not the ultimate answer. What we are all looking for is information about job growth. There are several competing sources using different methods and with different answers.

- ADP has actual, real-time data from firms that use their services. The firms are not completely representative of the entire universe, but it is a different and interesting source. ADP reports gains of 216K private jobs. Steven Hansen at Global Economic Intersection endorses the ADP method over the BLS result. He has a strong analysis covering many nuances in the data. For those who really want to understand the jobs story, it is well worth reading.

- TrimTabs looks at income tax withholding data. The idea is that this is the best current method for determining real job growth. TrimTabs forecasts gains of only 149,000, down from their revised January estimate of 181,000. (Their real-time estimate was for a gain of only 45,000, but they came forward and admitted a “calendar quirk” that threw off their forecast. There have been a number of changes in the tax withholding rules, so let’s cut them a little slack and give credit for being honest about what happened and their methodology. They provide a useful additional method).

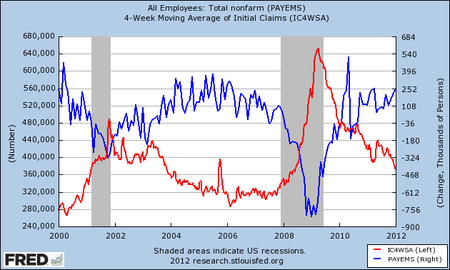

- Economic correlations. Most Wall Street economists use a method that employs data from various inputs, sometimes including ADP (which I think is cheating — you should make an independent estimate). I use the four-week moving average of initial claims, the ISM manufacturing index, and the University of Michigan sentiment index. I do this to embrace both job creation (running at over 2.5 million jobs per month) and job destruction (running at about 2.3 million jobs per month). In mid-year the sentiment index started reflecting gas prices and the debt ceiling debate rather than broader concerns. When you know there is a problem with an input variable, you need to review the model. For the moment, the Jeff model is on the sidelines.

Eddy Elfenbein has a similar idea. He looks just at initial claims and the employment report, and gets a very bullish result, a gain of 354,000 jobs. He finds a strong correlation over the last ten years, much better than I found in a longer time period when I built my model.

My guess is that this method is a little high, but I endorse the approach.

Conclusion

There was an excellent discussion of the ADP versus BLS issue this morning on CNBC. Joel Prakken, the Chairman of Macroeconomic Advisors is the featured guest, explaining how he has been so accurate in forecasting net job growth in recent months. The entire interview is interesting, and provides insight into how a top private economic modeling group uses data to improve estimates. Prakken is very practical in accepting that the recovery is only starting the long haul to regain 6 or 7 million lost jobs. He sees a job gain in line with ADP estimates (they helped to design those methods) and a downtick in the unemployment rate. Their data show that 125,000 jobs gained per month are necessary to tread water on unemployment, so anything above that makes some progress on reducing the unemployment rate.

Trading Implications

What does this mean for our trading and investing?

For investment accounts, I have been using the last two days as an opportunity to establish positions in favored names for new accounts and for enhanced yield while we can sell high volatility in calls.

For trading accounts it is reasonable to be more cautious. My experience is that you never miss much on employment Fridays. Even the strongest numbers get plenty of negative spin in the early going, that shorts can cover without much loss. You can count on Rick Santelli to check his email (as he did last month when the data seemed strong on all fronts) to learn what bloggers are saying about birth death adjustments, seasonal adjustments, labor force participation, or something similar. He will then explain why any progress can be characterized as completely bogus. These arguments might not prevail in the long run, but you only need a little time to get flat, and Rick has your back.

I make this observation not as a criticism, since everyone has a role and an audience. It is merely an observation about how this monthly drama plays out, told by someone who has watched it for many years. It used to be more dangerous to be short, but not so much in the age of the Internet.

If you agree with the thesis that the investing world is too bearish on the economy, there are many good leveraged plays for a rebound including CAT, CMI, and ATI [long all three.]